Jon Gormin – ORG

So – ’22 turned out to be an interesting year. We started the year bullish that it could be the year we return to normal after the pandemic. And today, it’s hard to believe a year ago I was still showing my vaccine card to get coffee in NYC and had to present a negative COVID test within 48 hours of returning to the US to gain re-entry. A lot has changed including the fact I’ve had COVID twice and received one more booster since writing my last Year in Review. But, as the year moved on, we moved into some sense of normalcy on a personal level. From a business perspective, it was much different. Just as it seemed like inflation could be abating, Russia invaded Ukraine. Commodities across the board spiked as a result of the invasion. Russia cut off its cheap natural gas to Europe and pessimists forecast Europeans freezing to death this winter and factories closing. The world was going to starve from a lack of Ukrainian grain, and new crops would be impacted due to a lack of Russian fertilizer. Fortunately, it hasn’t been as bad as predicted. Economically disruptive to be sure, but not economically catastrophic (to say nothing of the horrific humanitarian toll). However, it did keep inflation high and fears higher – so in came the Fed.

But before I focus on ’23, I want to reflect on my themes for ’22. Here were some of my key predictions from last year:

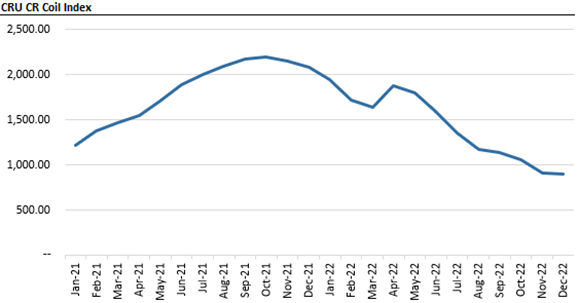

“Commodity prices and certain other inflationary trends should moderate in 2022” – excluding the blip from the war in Ukraine, this one came true. I can point to several datapoints, but one of the datapoints we track at one of our Partner Companies is steel prices.

As can be seen above, this steel index peaked in Q3 ’21 and, with the exception of the initial effects of the Ukraine war, has now come down below January 2021 levels. With some exceptions, many commodities look similar to the one above.

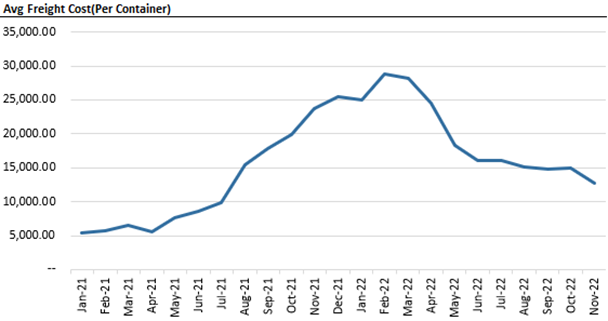

“Supply chains reach a new normal” – As I luckily predicted, supply chains improved dramatically in ‘22. The chart below is for a cost of a container from Asia for one of our Partner Company’s:

If the chart above continued past November, it would show that containers have continued to come down and are now at or below the January ’21 cost per container. We’ve also seen a significant reduction in the number of days at port and on the water that have led to further supply chain improvements.

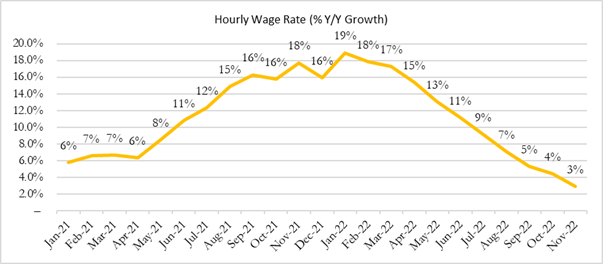

“In the short-term business owners are simply going to have to pay more for good talent.” – this was an understatement. Businesses needed to pay more for any talent as wages accelerated at a record pace in the first half of the year. Below is a chart from our Partner Company in the staffing industry:

As can be seen above, double digit annual year over year wage growth was the norm from June 2021 until May 2022. Just as a reminder, the Fed’s first rate increase was March ’22, its second was May ’22 and it ramped up to 75bp increases in June ’22. It looks like wages may be responding!

- “Getting and keeping talent will be a challenge for 2022” – hence, the Great Resignation. I wish I could have come up with that one!

- “Demand still seems strong” – which turned out to be the case for our Partner Companies. Every single ORG Partner Company showed revenue growth from ’21 to ’22.

In the rearview mirror, we hit all the key themes forecast for ’22. Demand stayed strong and revenue grew year over year. Wages kept increasing and finding talent was a challenge…until the very end of the year (but more on that later). Supply chains improved significantly and commodity prices moderated, albeit after a spike due to the war in Ukraine. 2022 ended up being a good year, but the Fed has taken the reins and is making a significant impact on the economy.

“Don’t Fight the Fed.” – Marty Zweig, 1970, Winning on Wall Street

As we look out to ’23, it’s hard not to think about the classic Wall Street line quoted above. You may not agree with the Fed, but they will win. After an unusually long period of time with loose monetary policy, the world changed in ’22 with the Fed aggressively boosting rates in the second half of the year. Unfortunately, it takes a while for the Fed’s tools to impact the economy, which is likely to impact ’23 (and probably part of ’24). But what will this mean?

The easiest thing to assess right now is that the Fed wants unemployment to go up. This is the only way for them to cool consumer demand effectively. Of course, they can’t say this but it’s clear they want entire, very large, segments of the economy to cool. Consumer goods, housing, autos will all cool in ’23 with many of them already in decline. Cash will be king and speculation will need a very high return to be justified (sorry tech folks). Right now, I don’t expect a strong recession. Maybe I am myopic, maybe I don’t live in Silicon Valley and see the technology bloodbath and maybe I live in Austin, Texas immune to the whims of Wall Street. That said – I have been in corporate finance for 30 years and I have never seen a severe recession move this slowly. Severe recessions come from shocks to the system – housing market collapses, sovereign country debt implosions, extensive broad-based speculation like the dot-com era. The US (and the Global economy) has been gorging on the free buffet of cheap money for over a decade and the Fed is putting us on a diet. Unfortunately, most of us have become used to eating whatever we want and the transition to fruits and vegetables won’t be enjoyable (albeit healthy!). It will be an uncomfortable transition, but good companies will be fine and position themselves to thrive down the road.

In 2023, I expect hiring to become easier for most industries and to provide the opportunity to prune underperformers (where before we just needed people to function!). I think wages will continue to moderate except for unique talent – which will continue to be in demand. I think we’re headed into a deflationary environment for most goods and maintaining your company’s margin dollars – not margin percentage – will be the challenge of ’23. For companies selling into the heavy construction, off-highway and agriculture markets, 2023 will continue to be good. There is still good market demand in addition to a lot of government money still waiting to be deployed. Business services companies may see a blip in their topline depending on end-market, but strong companies should be able to pick up customers as people look to reduce headcount and backfill these reductions through outsourcing. Overall, I believe that ’23 will be a challenging year for most businesses. I don’t believe we are going to fall off a cliff but only great companies will see a significant improvement over ’22 and I think it will get harder as the year goes on. Unfortunately, the Fed operates with a hatchet and not a scalpel, so the impact of their actions will take some time to impact the economy.

As for ORG, we expect good performance at our Partner Companies and are actively looking for acquisitions to continue to grow them during ’23. 2023 will probably be a good year to gain market share through acquisitions rather than through organic sales channels. We particularly believe strong companies should be aggressive in trying to capture market share (any way they can) from weaker companies that will need to retrench later this year. We are also looking for those great companies to partner with so that we can support their growth through ’23 and beyond. Warning: Shameless Plug If you are contemplating a partner in the next couple of years, we would love to talk to you and see if we can find a way to work together. Unlike other private equity firms, we don’t want to be your boss, but instead we want to work with you to co-author your journey.

I hope to see many of you this year as we try to figure out a way to work together, but if not we all wish you the best of luck in 2023 and we’ll see how my predictions fare in ‘24!

Sincerely,

![]()

Jon Gormin

Managing Director, Owner Resource Group