Doesn’t everyone love an election year?!? It always does a great job of stoking passionate political discussions, creating minor (and sometimes major!) freak outs, and providing uncertainty to the economy. Last year when I wrote my Year in Review, I ignored the election. Perhaps it was wishful thinking! Nonetheless, it’s behind us, there will be a new direction in ’25, and it’s time to refocus on the future.

So, how did ’24 turn out? As I have noted before, I only offer a biased perspective from the viewpoint of one person at Owner Resource Group. We primarily invest in business services and manufacturing companies. We don’t have any direct exposure to real estate, oil and gas or technology. We also focus on businesses that are classified by the financial community as lower-middle market….or generally companies with $30 million to $400 million of revenue. I highlight this only to let people know that our view is limited. This is not what you will read in the Wall Street Journal focusing on big companies, AI or rise of crypto. We focus on the ‘meat and potatoes’ of the US economy.

When I reflect on 2024, it was a mixed bag. From a financial performance perspective, our Partner Companies had uneven performance with 4 of 7 companies declining over the previous year. That said – the declines weren’t that bad and still felt good after the strong earnings growth of the prior years. In my 2023 Year in Review, I wrote:

“It’s a good time to focus on operational efficiencies and try to land new customers, but there will be very few markets with robust growth. I believe 2024 will set up for a much more exciting 2025 but we have to get there first!”

I think that turned out to be mostly correct. Growth with existing customers was slow or negative for most companies. Newly ‘won’ business was often delayed, forecasts were reduced, or the business was cancelled altogether. If you didn’t focus on your operations by improving efficiencies and reducing costs, 2024 was a weak year compared to its predecessors. But we’ve now made it through ’24 and I did say last year that ’25 is set up to be “much more exciting”…well, I might have missed this one since I don’t think it will be as exciting as I thought it would be a year ago.

On a couple other fronts – I think I did pretty well with my predictions:

“Hiring people will remain good relative to where it’s been in the past. If you are looking to upgrade talent or add positions, I believe that 2024 will be a good year to do that.” We saw this across our companies: open positions dwindled, hiring strong candidates improved and compensation ‘asks’ were acceptable. It was a nice change to be able to hire strong candidates to fill positions when needed.

“Inflation is behind us but won’t be going back to 2% for a long-time…and we can all survive just fine in a 3%-4% inflation environment.” Core CPI has stalled in the low 3% range. I don’t hear much chatter at Board meetings about inflation anymore. I think we are all surviving just fine. The crazy supply-demand imbalance of post-COVID has normalized. That said – we have entered a new geopolitical environment where the classic economic example of guns and butter won’t be as prevalent as the last 30 years. It could take a long time to get to 2% Core CPI…but I am not convinced it matters as long as we don’t have any major supply shocks.

“The financial community will loosen up in 2024 and this will improve as the year goes on. A big part of this will be finding price stability which will take time (ie – losses will need to be realized).” This did happen in 2024 – with lending coming back – but I still don’t think we’ve found price stability regarding private corporate valuations. In the private equity world, I learned a new term this year, ”Exit Ready Portfolio Companies”. What does this mean? Private equity firms have companies where they believe they have executed their strategy successfully so they are “exit ready” but they aren’t willing to sell. Why aren’t they willing to sell? They don’t like the valuations! Maybe valuations will improve…or maybe some investors will have to accept they overpaid and those assets might be “exit ready” but worth less than their underwriting cases. Then again, people may be willing to keep holding onto their portfolio companies for dear life as they have been and private equity portfolios will continue to keep aging until they are forced by their investors to do something!

For Owner Resource Group, 2024 was generally a good year. Although our Partner Companies had mixed performance, they were all well capitalized and able to continue to pursue their goals. Simply put…our stress level was relatively low. We did complete a significant, transformative acquisition for Standard Iron, Helgesen Industries, that positions the Company for substantial future growth. We also established new partnerships with Alliance Fleet (in the commercial vehicle upfitting industry) and Purpose Healing (in the mental health and substance use disorder industry) in 2024. We believe both Companies have exciting growth opportunities in partnership with Owner Resource Group for 2025 and beyond. Which brings us to 2025…

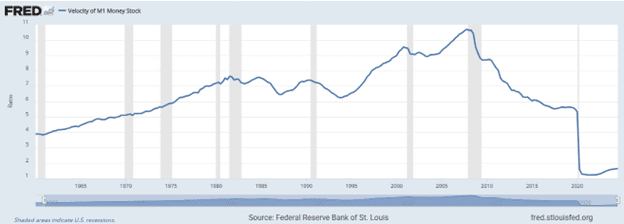

2025 is going to be an interesting year. One economic indicator that doesn’t get much airtime is the velocity of capital. Maybe I like it since I learned about it in Econ 101 and it ‘stuck’ but it seems very meaningful today. Below is a graph of the velocity of M1 supply since 1960 to today.

It’s a pretty amazing chart. Essentially, since COVID, the velocity of capital has remained at a 60 year low! There are lots of explanations – but without getting into minutiae – if the US economy could get back to its previous low point of approximately 3.8 then the velocity of capital would go up over 230%. Why does this matter? The more our money is changing hands and moving, the more economic activity is taking place. The economy works a lot better and is a lot more fun when money is moving quickly. Since the bottom, the velocity of capital has increased over 30%, but it wouldn’t be unusual for it to go up another 100% from where it is today. If this occurs, the economy will feel a lot better.

In order for this to happen, transaction activity, new construction activity, capital expenditures – all of these need to improve. The lending market has reopened. It is not robust, but it is adequate. For this reason, I am optimistic about the outlook for the US economy, but I don’t believe it will be robust in 2025.

As I look at our companies, very few of them are willing to budget robust growth in 2025. Our companies almost universally work with larger businesses who are providing them forecasts that are modest at best. I believe most people expected 2024 to be a better year, put together budgets that showed solid growth, and were burned by it. Heading into 2025 people are being more cautious. I also don’t see a quick ‘risk on’ scenario driving activity. Will the Trump policies be beneficial or detrimental? It is hard to determine but it is unlikely that any of them unleash a torrent of economic activity in ’25. Perhaps they will position the economy for strong growth in ’26, and I expect the economy we live in to improve throughout the year, but I don’t see anything that suggests an economic breakout in ’25.

I also believe that ’24 was our first ‘normal’ post-COVID year competitively. After wild swings in supply and demand post-COVID, most markets seemed to have found balance by the end of ’24. The problem with balance is that we’ve returned to normal levels of competition where simply providing the product or offering is no longer enough. For most businesses it’s been almost five years since they lived in a normal environment. Competition is real. Pricing pressure has returned. If you cannot differentiate yourself from your competition, you will have continued pricing pressure in ’25. Welcome back to the real world!

Along these lines, we have voiced this opinion to our Partner Companies. We believe it is prudent in ’25 to focus on operational efficiencies and actions within your control. Market share will be harder to capture but there needs to be a significant emphasis on new business. This will position companies to capitalize on future economic strength. Acquisition activity will continue to expand in ’25 although valuations will likely remain muted (albeit improving) for most, if not all, of the year. 2025 should be a good year for expanding your business through acquisition since many companies have had peak earnings and will be facing a more difficult environment. As a result, selling or merging with a competitor will make more sense financially for both companies than it has over the last several years. Hiring should remain good throughout the year – and I recommend people make their critical hires in the first half of ’25 just in case the market tightens later in the year. The policies of the new administration will have an impact, but making a prediction on the direction and outcomes would be purely speculative. Some of them may even offset each other and result in not much change in ’25, but end up impacting certain industries disproportionately to others. So – my punchline for ’25 is to prepare for ’26…and pray for an acceleration in the velocity of capital. It makes everything so much more fun!

Of course, if you are looking for a partner to grow your business, please reach out to any of us at Owner Resource Group. We only look to partner with 2 or 3 business owners a year that want to remain significant shareholders with a private equity partner that can help them grow their business significantly. We have a 17-year track record of providing the resources and capital – in a collaborative manner – to support breakout growth. Earnings at our companies have grown over 230% and employee growth has exceeded 100% during our partnerships. And, most importantly, we do it the right way with trust and transparency every time. I hope everyone has a prosperous ’25!