![]()

Owner Resource Group is pleased to provide the following wealth management insights from Round Table Wealth Management

First Quarter 2022 Review

Before we dive into our quarterly letter, we would like to express our ongoing concern and hope for a peaceful settlement for the people of Ukraine. May our world leaders find resolutions to fortify a lasting peace.

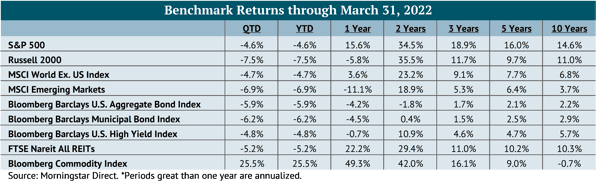

Capital markets retreated in the first quarter, not at an alarming rate, but certainly a deviation from the pattern of positive quarters investors have grown to appreciate. Of the last 50 quarters since the Great Financial Crisis, only 8 quarters generated a negative return and nearly all these quarterly drawdowns were recouped within the following quarter. The most important factor impacting markets during the first quarter was the prospect of continuing rising inflation and the certainty of rising interest rates. While the equity markets rallied into quarter-end, Federal Reserve Governor Brainard (historically a very dovish member of the FOMC) and subsequently the Fed’s minutes stated that it may “rapidly” reduce its balance sheet starting in May, which fostered a selloff in both equity and bond markets.

Our portfolio positioning during the quarter increased exposure to liquid hedged equity, reduced growth-style investments and further reduced longer-duration fixed income. We maintained exposure to commodities, which have performed admirably this year. Recent inflation figures suggest the increase in consumer prices is not over and the Federal Reserve is nearly certain to continue its rate increase strategy. Chairperson Powell mentioned the Fed’s ability to increase rates by 50 basis points (similar to when he discussed a 25 bps increase prior to the official March announcement), which could be viewed as Powell giving the market “long headlights” to see the rate path ahead. Since the market lows in early-March, growth-style valuations have increased back to significant premium valuation levels. Combined with the path of interest rates, increasing inflation and the ongoing conflict in Ukraine, we are maintaining our current allocations with a greater emphasis on hedged equities.

The Big Picture

The U.S. economy generated real gross domestic product growth (GDP) of 5.7% in 2021 and was expected to grow 1.8% in the first quarter of 2022. Many economists were surprised when the initial reading of first quarter GDP growth registered a negative 1.4%. The dramatic change in outcome was primarily due to a material increase in net imports, which detract from GDP. On the positive side, consumer spending was rather strong. Looking forward, issues such as inflation, higher interest rates and employment costs will be closely monitored by the Federal Reserve as they attempt a “soft landing” for the U.S. economy as it transitions out of easy-money policy. While the near-term GDP outlook has been tempered, there remains an optimistic view for the second quarter of 2022 with a projected GDP growth rate of 4.7% and, ultimately, anticipated 3.7% U.S. GDP growth for calendar year 2022. We suspect some adjustments may be forthcoming.

Global economic growth for this year is expected to be 3.5% based on projections by Fitch. In the same report, the Eurozone, not surprisingly, had its economic growth reduced by 1.5% to 3.0% considering economic complications from the Ukraine/Russia War. The Eurozone’s largest economy, Germany, is heavily dependent on Russian oil and natural gas, the latter of which accounts for 40% of its supply. According to Bloomberg, about 50% of homes in Germany are heated with natural gas and a large swath of industry is beholden to gas for manufacturing. Higher costs in Germany, which is a large exporter to China, will likely (ultimately) be reflected in higher prices (inflation) in the U.S. This has fed into weakening consumer confidence, as the European Commission’s consumer sentiment index fell to its lowest level since April 2020, the height of the pandemic.

U.S. inflation based on the differential between nominal U.S. Treasury Notes and U.S. Treasury Inflation Protected Securities is expected to average about 4.3% and 3.4% over the next 2-years and 5-years, respectively. Our outlook is that inflation, interest rates and the War will continue to have a dampening impact on capital markets in the near term. Any indication of any of these factors easing will likely be met with a drop in market volatility measures and rising share prices. We witnessed this several times this year on news of potential negotiations between Ukraine and Russia.

Rising inflation and the Ukraine War has driven the commodities market skyward. The notable aspect of commodity markets is the marginal unit; when marginal demand is not met by marginal supply, prices go up. For example, in crude oil, a global commodity, Russia produces 10% of global supply. The sanctions placed on Russia removes many of those barrels from satisfying demand, and consequently the world becomes very short of oil barrels, very quickly. Global oil prices jumped on news of Ukraine and remain around $100/barrel today. Other commodities such as wheat (Ukraine supplies about 10% of global wheat), nickel and fertilizer all are experiencing supply deficits, which is driving prices of these commodities higher. We expect that these dynamics will find their way into everyday consumer prices, which were already impacted by global supply chain issues. An adage in commodity markets states that “nothing cures high prices, like high prices” meaning the current high commodity prices will ultimately lead to greater production, which satisfies demand, and eventually lowers prices. For consumers and the Federal Reserve, this couldn’t happen fast enough.

While the market focused on geopolitical and macro risks, financial analysts did something that many investors did not anticipate– they raised S&P 500 FY2022 earnings estimates. If current earnings estimates materialize for the S&P 500, the result will be a 2022 earnings growth rate of 16.2%. Even greater growth is expected in U.S. small cap. The S&P 500 Equal Weighted Index (the largest company in the index is held at the same weight as the smallest company) highlights projected 2022 earnings growth of 25.8%. Current estimates combined with stable valuations imply strong returns for this year, but our view is more tempered. There remains plenty of time for earnings estimates to change prior to year-end. Issues to consider include the pace of consumer spending in the face of higher prices as discussed above. Everyday purchases such as gas and food are up materially and are expected to remain so for the foreseeable future. Thus far higher prices have not negatively impacted the strong growth in consumer spending, which translates into company earnings, but we are watchful of signs the trajectory is turning. Consumer confidence recently surprised above economic estimates, but remains well below pre-Covid levels. We believe equity markets could end the year on a positive note, but we maintain hedged equity exposure due to potential “tail risk” events and value-style investments with lower relative valuations.

Bonds are not providing the “safe haven” investors expect. During the first quarter the Bloomberg U.S. Aggregate Index (a proxy for the broader U.S. bond market) was down 5.9% and the Bloomberg Municipal Bond Index was down 6.2%. The simple explanation for this is bond math. As market interest rates increase, bond prices decline to allow for a given bond’s yield to come back into equilibrium with the market rate. (The opposite held true in 2020 as market rates declined). This dynamic has a compounding effect on those bonds with longer duration (found in the Bloomberg U.S. Aggregate and Municipal indices) as the larger number of future coupon payments are discounted at a higher interest rate, reducing their present value and the bond’s market price. (This same math applies to high growth companies whose large projected cash flows are further out in the future). In contrast to fixed rate bonds that largely comprise the Bloomberg U.S. Aggregate, floating rate loans have interest rates that reset as market rates increase (or decrease) alleviating much of the interest rate risk of fixed rate bonds. We will continue to hold shorter-durations bonds subject to a client’s immediate liquidity needs.

The Outlook

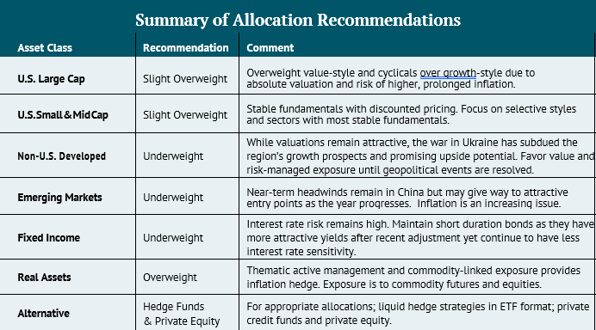

We continue to hold a slight overweight to U.S. Large Cap equities. The large cap asset class captures several attributes we believe are important given the state of geopolitics and macroeconomic factors. First, U.S. large cap companies continue to have strong balance sheets and by their status, more commanding market positions. For example, the S&P 500 in aggregate has a net debt to EBITDA ratio of 0.98x at YE 2021 and a projected FY 2022 ratio of 0.88x. These ratios are the lowest since 1995. Large cap’s position of strength can provide shareholder friendly financial strategies such as share buybacks, accretive acquisitions, and the capacity to adjust supply chains that reduce longer-term business risk. Within the large cap asset class, we are maintaining our bias to value-style investments driven primarily by our valuation concerns. Value, vis-Ã -vis the Russell 1000 Value Index is trading at a modest premium to its 10-year trailing price-to-earnings ratio, while its growth counterpart is trading at a valuation representing a 35% premium. The premium valuations in growth-style investments are at risk given the Federal Reserve’s focus on inflation and the growing chorus of economists calling on the Fed to be more aggressive against inflation.

We maintain a slight overweight recommendation to the small and mid-cap asset class as the relative fundamental backdrop remains supportive. While the Russell 2000 Index suffered a nearly 10% drawdown in January as the market priced in a faster and more aggressive rate rising cycle to combat inflation, it made up some ground as the quarter progressed. SMID Cap, like much of the U.S. equity market, eventually shook off geopolitical risks associated with the Russian invasion of Ukraine. Earnings expectations jumped around during the volatile quarter, but changes were relatively muted and calendar year earnings expectations were 2% higher at quarter-end for the S&P 600 Index compared to where they started the year. Overall earnings growth is still anticipated to be over 19% this year for the S&P 600 Index as of early-April according to Bloomberg. However, the disruptions from the war in Ukraine will undoubtedly impact the global economy and the small cap universe despite very little direct exposure to the region. We are less concerned about this impact as the asset class is in a strong position to digest disruptions but would not be surprised to see calendar year earnings come in as the year progresses. As such, during the quarter, we increased exposure to areas where we see less risk of downward earnings revisions like value sectors and have reduced the growth exposure where downward earnings revisions have already started. Year-to-date, small cap sectors like consumer discretionary and technology have experienced a decrease in earnings expectations as GDP estimates were revised lower while other sectors like materials and energy have seen earnings expectations increase due to global commodity supply chain disruptions brought on by the war iin Ukraine.

We recommend an underweight allocation to international developed market equities. Developed markets fell 4.7% during the quarter, which was roughly in line with the S&P 500. International markets experienced a more pronounced drawdown in the back half of the quarter due to Russia’s invasion of Ukraine, particularly Europe due to the region’s dependence on Russian natural gas and oil. As a result of the ongoing conflict, the economic outlook for international markets has been reset at a time when economic activity had been steadily improving over the last year. In Europe, where natural gas prices have nearly doubled over the last month and inflation is at record highs, the economy is likely to retreat from recent levels. While economic growth is expected to remain positive, it has been noticeably reduced. According to Fitch, European GDP growth for 2022 has been revised down from 4.5% to 3.0%. Surging inflation has also spurred the European Central Bank to accelerate policy tightening by ending bond purchases in Q3 and expectations that rate hikes may begin in early 2023. These tightening actions as well as the pace of tightening could add further constraints to future economic growth in the region. In recent weeks, we reduced our allocation to growth in favor of adding dedicated value and hedged equity exposure in the asset class.

In emerging markets, we also hold an underweight allocation to the asset class. Emerging markets declined 6.9% during the first quarter, dragged down by the conflict in Ukraine. The widespread condemnation and sanctions against Russia resulted in Russian equities becoming effectively uninvestable for foreign investors. As a result, Russia has been broadly removed from emerging market indices, even though the country only comprises less than 4% of these market benchmarks. Performance across the rest of the asset class has been varied. In China, markets pulled back 14.2% during the first quarter, and are now down 32.5% over the trailing one-year. Chinese equities were most recently unsettled after the SEC named five companies under scrutiny for potential delisting if they failed to meet U.S. listing audit requirement, sparking concerns over the future of Chinese companies remaining listed on U.S. exchanges. Chinese regulators were quick to respond and alleviate fears, stating that they are working with their U.S. counterparts to resolve the audit dispute as well as signaling that the campaign of regulatory crackdowns was nearing its end. Additionally, increased monetary easing in China is anticipated throughout the year to combat a softening economy. Elsewhere, the boom in commodity prices has been a welcomed respite. Resource-driven economies, such as in Latin America and South Africa, have posted positive performance year-to-date and are noticeably outperforming the rest of the world. During the quarter we reduced the overweight to Asian emerging markets in favor of a more balanced regional allocation.

We increased our underweight to fixed income during the quarter as it became clearer that the Fed intends to be more aggressive in raising the Fed Fund Rates and reducing their balance sheet as compared to past rate rising cycles. While our allocation was biased towards short-duration strategies to mitigate the impact of higher rates, we further reduced intermediate exposure held in portfolios where rate risk was the highest. We continue to find the below investment grade floating rate loan universe to have the most attractive attributes in the current environment due to stable corporate fundamentals and insulation from rate risk.

We are maintaining client portfolio exposure to real assets/commodities via liquid exchange traded funds and mutual funds. While it is true that many commodity prices hit recent record highs during this past quarter following the invasion of Ukraine, future upside in commodity prices is not contingent on prices getting back to these record highs. Rather, prices would only need to stay elevated as the futures curves suggest lower prices in the future. Given the lack of progress towards a resolution and damage done to international relations even if a resolution is agreed upon, a higher for longer scenario appears to be more and more probable in the commodity complex.

*The content herein is provided to you by unaffiliated sources believed to be reliable, but not guaranteed on an as-is basis without any warranties of any kind. In no event shall Owner Resource Group, LLC be liable for any direct, indirect, incidental, punitive, or consequential damages of any kind whatsoever with respect to this content. The content is distributed for informational purposes only and not intended to provide investment advice. The information contained in this article is accurate as of the data submitted, but is subject to change. We strongly recommend you consult your professional business advisors before making any financial or investment decisions.