![]() Owner Resource Group is pleased to provide the following wealth management insights from Round Table Wealth Management.

Owner Resource Group is pleased to provide the following wealth management insights from Round Table Wealth Management.

Fourth Quarter 2020 Review

We would like to first acknowledge and offer our heartfelt condolences and thoughts to those that lost loved ones or suffered economic hardship during this ongoing pandemic. It was a year like no other. Winston Churchill once said, “If you are going through hell, keep going.” We agree: stay safe, stay positive and keep moving forward. We hope you had a reflective New Year’s and join us in looking forward to 2021 and beyond.

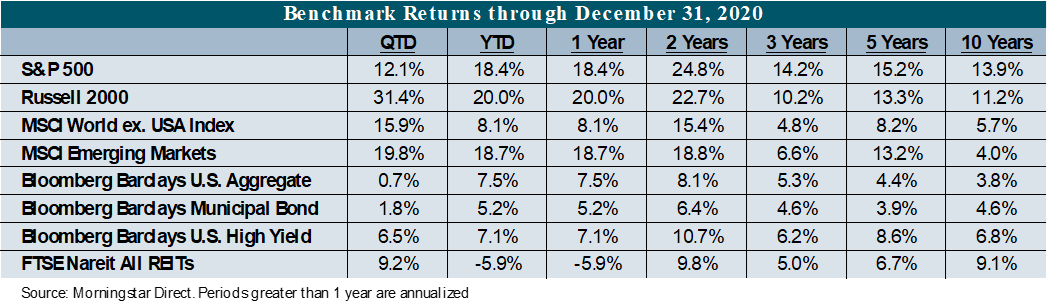

Despite the economic lockdowns of 2020 and emotional hardship, the capital markets performed admirably with the S&P 500 increasing approximately 18.4% by year-end and nearly all equity styles generating positive performance. Many of the risks that we highlighted throughout 2020 have dissipated: COVID-19 vaccines are being developed and deployed, stimulus measures are being passed to provide necessary funds for families across the country and the Presidential election has been decided and finalized. We are currently more optimistic than we were at this time last year and will remain constructive on markets near term. We are pleased with the performance that client portfolios generated and the tactical maneuvers we initiated to manage risk at the most concerning of times. Today, portfolios are largely unhedged as we are cautiously optimistic entering 2021.

The Big Picture

The U.S. economy is expected to grow by approximately 4% in 2021. Several catalysts support this projection, including improving and more widespread availability of COVID-19 vaccines and additional stimulus measures on top of the recent $900 billion Federal stimulus passed in December 2020. The administration has communicated its preference for an increase in economic impact payments to individuals to $2,000 from $600. As discussed in a prior letter, recipients of initial economic impact payments in April 2020 used those funds to make purchases, which ultimately helps to keep the economy primed and helps to bridge the economic chasm caused by the pandemic.

With Democratic party control over both houses of Congress, the Biden administration has a pronounced ability to pass additional stimulus and infrastructure spending, to alter tax policy and to administer new regulations. Not all platform initiatives will be a “slam dunk.” Moderates abound in the Democratic party, making some legislation easier to pass than others, but largely our expectation is for vast amounts of liquidity entering the U.S. economy.

Federal spending will have many positive benefits, such has helping small businesses, families and the unemployed. The potential economic risks of increasing Federal spending include substantially higher Federal debt, a declining U.S. Dollar relative to other foreign currencies and the potential for inflation to increase faster than anticipated. The colloquial cause of inflation is “too many dollars chasing too few goods,” which could happen as a massive amount of liquidity is injected into the economy. We recognize that inflation may also be “imported,” meaning the declining U.S. Dollar makes imports more expensive on a relative basis, which causes the inflation rate to increase. The Federal Reserve has communicated its desire for inflation to average 2% over a market cycle, but should inflation increase faster than expected, the possibility of the Fed raising rates becomes more relevant. We are reminded of the Taper Tantrum that rattled markets in 2013 as the Fed simply stated it was thinking of raising rates. As 2020 demonstrated, remote possibilities are nonetheless possible and the aperture focusing on potential outcomes requires widening.

The Outlook

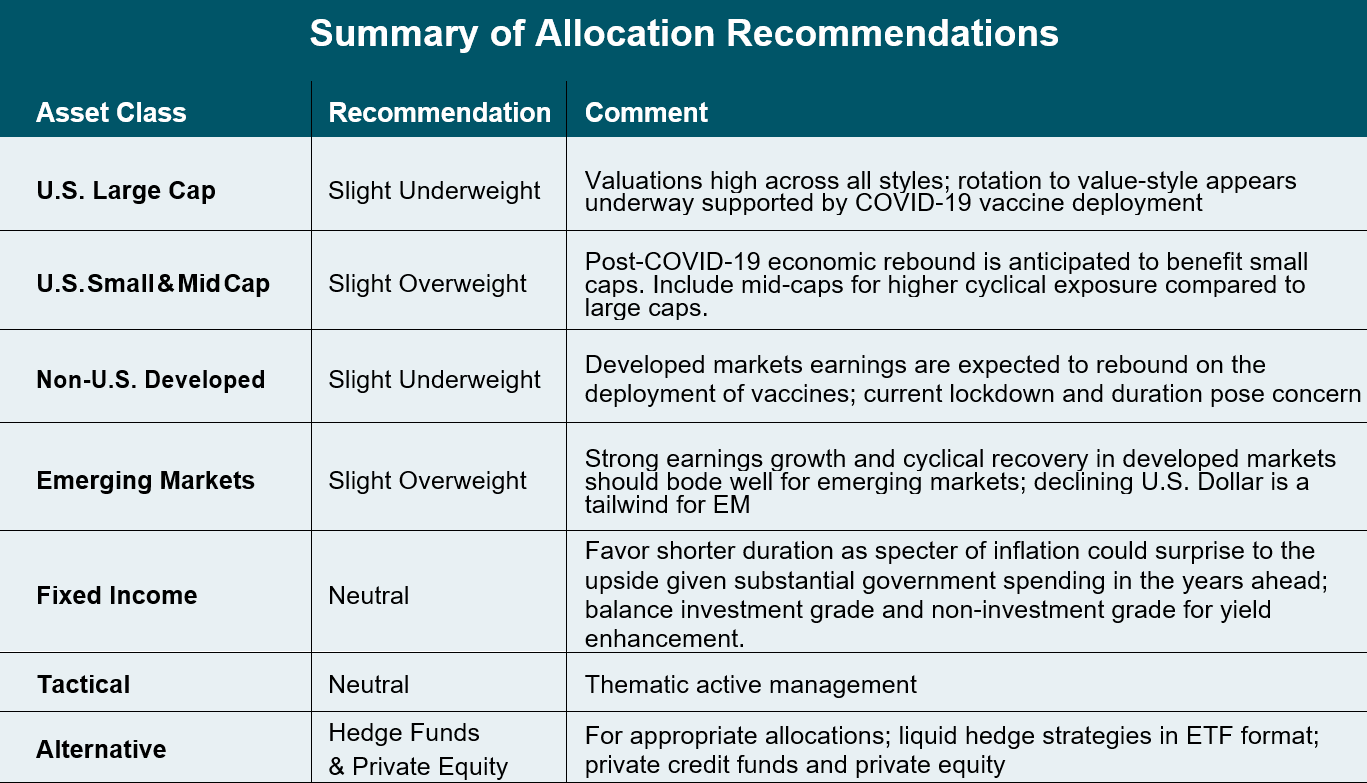

We hold a slight underweight to U.S. Large Cap, with an emphasis on value-style over growth-style investments. Growth investments have dominated over the last several years, but since October 2020 a rotation to value-style investments has developed, which we believe may continue as COVID-19 vaccine distribution increases. On an asset class basis and using the S&P 500 as a proxy, large cap companies are projected to increase earnings by approximately 31% and 17% in 2021 and 2022, respectively. We believe these growth rates are achievable given that 2020 earnings fell 17% due to the pandemic, creating a low threshold for growth in 2021. In addition to earnings, a successful year ahead in large cap equities will be influenced by the extent to which companies are able to maintain their historically high valuations. Growth-style investments are most at risk, while value-style investments are less at risk on a relative basis. We believe valuations may maintain levels for several reasons. First, relative return opportunities outside of equities are scarce as fixed income yields are miniscule and any elevated expectations of future inflation will negate returns. Second, investor cash balances remain high with approximately $4.3 trillion invested in institutional and retail money market funds. These funds pay close to zero interest rates, making the S&P dividend of 2% quite attractive on a relative basis. Lastly, corporate balance sheets are flush with cash. Companies will feel pressure to put capital to work either through share buybacks or acquisitions, both of which should be beneficial for investors.

We have a slight overweight allocation to the SMID Cap asset class with a neutral allocation to small caps and an overweight allocation to mid-cap exposure to capitalize off a cyclical recovery. After such a strong rally from market lows and a positive return of 20% in 2020, many investors are likely questioning the ability for the rally to continue within small caps. However, YTD returns suggest the trend is continuing with small caps up nearly 6% in the first week of 2021 compared to less than 2% for large caps. We continue to believe that the small cap rally could continue and point to a variety of factors that can help drive positive returns in 2021. First, the cyclical recovery is poised to continue as inventories are rebuilt across the economy. This will likely be a multi-quarter event that will help aid in small cap fundamental growth. Second, while the rebound has been fast and fierce, the cycle is likely not over. According to Royce Investments, over the last 12 small cap cycles, the peak-to-peak return has averaged 44%, but as of year-end, small caps sit just 17% above their prior peak. Third, valuations within small caps are at less extreme levels compared to large caps, so even if interest rates rise, the asset class may be more insulated from this risk. Similarly, the equity risk premium (defined as free cash flow/enterprise value less the 10-Year Treasury yield) is elevated within small caps and it has only recently retreated from the upper range of 2%. Past periods of this metric reaching 2% were in times of economic stress like 2009, 2011, and 2016 before it reverted to 0%.

We recommend a neutral to slight underweight allocation to international developed market equities. Dissipating risks, from the U.S. election to vaccine developments, pushed global equity markets higher in the fourth quarter and as we look forward to 2021 our outlook toward non-U.S. developed markets has incrementally improved from previous quarters. With the rollout of a COVID-19 vaccine, a sustained global economic recovery should give way to a rotation back into value-oriented sectors, providing a relative benefit to Europe and Japan compared to the tech-driven and more growth-oriented U.S market. These expectations have manifested in the resurgent earnings growth forecasts for the developed region, namely Europe. According to JP Morgan, European earnings are forecasted to grow 37% in 2021, noticeably outpacing current U.S. estimates. Domestic and cyclical sectors that were hampered during 2020 are anticipated to contribute the overwhelming portion of the earnings growth in 2021. Specifically, the financials, industrials, energy and materials sectors are expected to contribute over 60% of the total earnings growth in Europe, a significant reversal from what occurred last year. Finally, with risk appetite returning to markets and an improving outlook, it is anticipated that investors will reposition back into developed market equities, which has been weighed down by steady outflows over the past two years. That said, we believe the newest round of COVID lockdown measures within Europe may continue to weigh on investor sentiment over the near-term.

Within emerging markets, we recommend a slight overweight allocation. Emerging markets experienced a strong rally into the end of 2020, returning 19.8% during the fourth quarter. 2020 returns in emerging markets were focused in Asia as the region’s COVID response and growth-oriented economy outpaced other EM regions. In particular, China and its tech-driven equity market returned 29.7% in 2020. We retain a positive outlook toward emerging markets based on a few compelling drivers. EM earnings for 2021 are anticipated to grow at 34% driven by a reflationary environment. Given the cyclical nature of certain EM regions and countries such as Brazil, Russia and Mexico, a synchronized global recovery will likely benefit emerging markets. As a result, compared to the Asian-focused returns in 2020, performance in EM may be more widespread going forward. Additionally, a weaker USD would further aid emerging markets and is supported by easing trade uncertainty from a Biden presidency and improving global growth prospects.

We maintain our neutral weight allocation to fixed income with an emphasis on shorter duration strategies. Fixed income returns were mixed during the quarter as Treasury rates drifted higher following the Presidential Election, resulting in a return of -0.8% for the U.S. Treasury Bond Index. However, most other areas of the fixed income universe generated positive returns as spreads compressed within higher risk areas. High yield and emerging market bonds outperformed with returns of 6.5% and 4.5%, respectively. Investment grade corporate bonds also rallied with a return of 3.1% for the quarter, rounding out a nearly 10% year-to-date return. Municipals also benefitted from the Presidential Election outcome and the asset class rallied 1.8% during the quarter as yields normalized to that of Treasuries due to expectations of higher tax rates and more federal support for local and state municipalities. With the 2-Year, 10-Year and 30-Year Treasury rates closing the year at 0.12%, 0.91% and 1.64%, respectively, the concern going forward is inflation. Inflation expectations and breakeven thresholds have breached 2% for the first time since March and, if the trend continues, it may force the Fed to reverse their accommodative positioning earlier than they have previously communicated.

Tax and Financial Planning News

With the 2020 election coming to an end and the Democrats taking control of the Senate, the House of Representatives, and the Presidency, many policy experts expect tax policy to change in significant ways. Throughout the campaign, the Biden administration proposed several tax-policy changes that we believe are likely to focus on personal income tax rates as well as corporate tax rates. Biden has proposed raising the top personal income tax rate from 37.0% to 39.6% for those making over $400,000 per year. The corporate tax rate, which was cut to 21% under the Trump administration, is expected to be increased to 28%. Other tax changes under the Biden proposal include expanding the 12.4% social security payroll tax on income over $400,000, currently capped at $142,800. This would be split between employer and employee and would result in no social security payroll tax on income between $142,800 and $400,000. In addition, it is expected that the current federal estate tax exemption of $11,580,000 will be reduced to between $3.5 million to $5.0 million per individual. One uncertainty that investors face today is when these tax changes will take place, if passed. Many believe tax law changes would be retroactive to January 1, 2021, while others argue they would be delayed until 2022 as the country recovers from the COVID-19 pandemic.

Regardless of timing, we believe investors and business owners should begin preparing for higher taxes in the future. Business owners may want to look to qualified retirement plans as a way to maximize savings and investments, while decreasing their taxable income. While many business owners are familiar with 401(k) and profit-sharing plans, a Cash Balance Plan can also be an extremely valuable savings vehicle for owners and partners who are looking for larger tax deductions and accelerated retirement savings. For example, a 55-year-old would be eligible to contribute upwards of $200,000 into a Cash Balance Plan on top of the maximum defined contribution limit of $64,500 for the tax year 2021. Because a Cash Balance Plan is a pension plan with required annual contributions, consistent cash flow and profit is very important. Before starting a Cash Balance Plan, please speak with your Round Table Wealth Advisor.

*The content herein is provided to you by unaffiliated sources believed to be reliable, but not guaranteed on an as-is basis without any warranties of any kind. In no event shall Owner Resource Group, LLC be liable for any direct, indirect, incidental, punitive, or consequential damages of any kind whatsoever with respect to this content. The content is distributed for informational purposes only and not intended to provide investment advice. The information contained in this article is accurate as of the data submitted, but is subject to change. We strongly recommend you consult your professional business advisors before making any financial or investment decisions.