![]() Owner Resource Group is pleased to provide the following wealth management insights from our partners at Round Table Wealth Management.

Owner Resource Group is pleased to provide the following wealth management insights from our partners at Round Table Wealth Management.

Third Quarter 2020 Review

“It was the best of times, it was the worst of times, it was the age of wisdom, it was the age of foolishness, it was the epoch of belief, it was the epoch of incredulity, it was the season of light, it was the season of darkness, it was the spring of hope, it was the winter of despair.”

– Charles Dickens, A Tale of Two Cities.

We think this quote by Charles Dickens in many ways sums up the current financial and economic environment and certainly reflects the partisan politics of the day. In client conversations, one of the most frequently asked questions is, “How is the market doing so well, while the U.S. economy remains so fragile?” It’s a very appropriate question that we will address in this letter, but in short, when trillions of U.S. Dollars are pushed into the financial system, asset prices will almost surely increase: think stocks, bonds, and homes. So, in the Dickensian sense, for financial and real assets it’s the best of times, but for certain industries and the millions of unemployed it remains the worst of times.

Our investment approach to managing risk through these unprecedented times has been more tactical than usual. In “normal” market environments, we seek to manage risk in line with a client’s strategic long-term asset allocation, which usually consists of unhedged equity exposure for growth and an appropriate allocation to fixed income and cash for income and stability. Today’s market poses challenges to historical risk management techniques, as interest rates are at historically low levels and high bond prices offer marginal upside to offset potential equity price declines. Consequently, where appropriate we have implemented hedged strategies across equity allocations to limit drawdown risk, while also providing the opportunity for modest upside should the equity markets continue to trend higher. We cannot know whether it’s the best of times or the worst of times until after the fact. We do believe, however, that these times are laden with greater uncertainty and for that reason we have temporarily increased the use of hedged strategies.

The Big Picture

U.S. real gross domestic product is expected to advance at an annualized 19.1% growth rate in the third quarter of 2020 versus a revised annualized decline of 31.4% in the second quarter. The third quarter estimate is a significant increase from the prior estimate of 10.6%, but may be influenced by the expectations for another round of fiscal stimulus. The on-again / off-again nature of negotiations between House Speaker Nancy Pelosi and Treasury Secretary Steven Mnuchin has led some economists to qualify estimates subject to additional stimulus legislation approval. Ultimately, some forms of stimulus measures are likely, but the timing and magnitude of an agreed upon package is uncertain. As we look toward 2021 and 2022, economic growth is expected to return to the +3% range.

While further fiscal stimulus remains uncertain, monetary stimulus has provided much needed support and the Federal Reserve is going above and beyond past actions to keep the economic recovery intact. The Fed is expected to maintain its ultra-easy monetary policy through at least 2022. This observation is based on the Fed’s updated inflation outlook, which suggests inflation will not reach the targeted 2% threshold until December of that year. Fed Chairman Powell also stated that the Fed will target an average inflation rate of 2% over a market cycle going forward rather than a hard 2% level. This shift in policy suggests that inflation will be allowed to run above 2% for an extended period of time before the Fed increases rates, indicating that rates will likely remain low beyond 2022.

Capital markets are benefiting from these low rates as investors have increased their willingness to pay high valuation multiples. As we’ve discussed before, equity share prices are premised on the value of future cash flows generated from a business. Those cash flows are discounted at an interest rate and then added up to ascertain the value of a company’s equity (its net present value). A high interest rate lowers a company’s net present equity value, while a low interest rate increases its net present value. In the current environment interest rates are very low! Consequently, net present values of share prices have increased and equity valuation multiples are the highest they have been in decades. Certainly, this is the best of times for shareholders! As we stated above, the Fed is likely to keep rates low for a prolonged period of time. Therefore, from an interest rate perspective it is plausible that the market can continue to maintain its current high valuations. But it’s never that easy–.

Despite the market’s resiliency, “worst of times” risks remain. The economy remains fragile and over 11 million people remain without employment. Compounding this dynamic are concerns around housing evictions, the impact on small businesses given limited “opening” regulations (small business employs 40% of the workforce) and the potential for a second COVID-19 wave (surprisingly though, recent regional infection spikes have not resulted in market drawdowns). Fiscal policy has helped alleviate a situation that could have been much worse, but as Jerome Powell stated in his recent testimony, and supported by other regional central bank governors, the U.S. economy remains weak and needs additional fiscal policy support; the Federal Reserve can’t do it all alone. The capital market has been able to recover as it anticipates monetary policy and fiscal policy will ultimately move forward to provide support to those in need. In fact, both Democrats and Republicans believe a stimulus measure is needed, they just can’t agree on the amount. This latter point gives us concern as we move closer to the election that is only a few weeks away. With partisan politics reaching a feverish pitch, we believe there is a high probability of market gyrations in the near term until the election is resolved and stimulus legislation is approved. Subsequent to this outcome, we believe market uncertainty could decline as unknowns become knowns, stimulus measures are approved and businesses can plan accordingly.

The Outlook

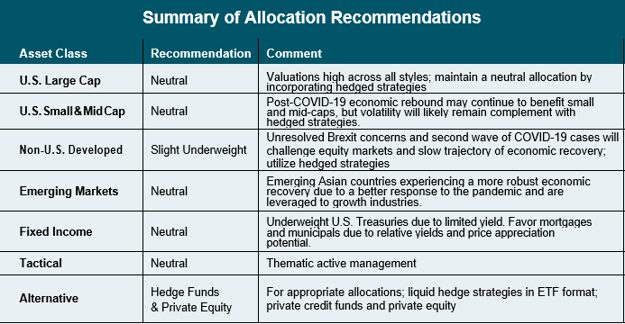

We maintain our neutral view on U.S. large cap equities. S&P 500 earnings estimates for 2020 have been trending favorably and imply earnings growth of over 20% for the next two years. The key concern remains equity valuations that are historically high. Should valuations remain constant, then implied returns are quite strong, but we are reluctant to base a recommendation on the willingness of other investors to pay ever higher valuation premiums. In the near-term, we are maintaining a neutral allocation by incorporating a hedged strategy that is expected to limit downside should a market sell-off develop. Looking further ahead, despite growth-style investing remaining the dominant market driver today, we anticipate value-style investments to gain support next year as both Democrats and Republicans favor significant infrastructure spending that will boost fundamentals of many value-style industries.

We maintain our neutral view to small caps. Despite fundamental data improving for small caps, sentiment remains more pessimistic relative to their large cap peers. According to Yardeni Research, the S&P 600 traded around a 19x forward earnings multiple near quarter-end, which is at the upper end of its historical range, but a bargain compared to the approximate 21x forward valuations on the S&P 500. While large cap’s premium may have been warranted given their ability to better weather the COVID-19 storm, as the storm passes, small caps are poised to see a greater sensitivity to an economic growth environment. As such, we maintain our small cap exposure at a neutral weighting and complement it with mid cap exposure, resulting in an overweight to mid cap within the asset class.

We recommend a neutral to slight underweight view to international equities, but favor hedged equity exposure to manage the downside risks in equity markets globally. Within developed markets, we have been encouraged by the 750 billion Euro stimulus package passed by the European Union (EU) in July as well as positive economic activity data indicating an initial recovery. Additionally, the asset class has benefited from a weakening U.S. Dollar, which contributed 3.4% to non-U.S. developed market returns during the quarter. It is anticipated that

U.S. Dollar strength will be contained through the end of the year given that interest rates in the U.S. will remain low and the uncertainty around the election has motivated investors to unwind safe-haven U.S. Dollar assets. However, developed markets still exhibit noticeable risks. While the U.S. Presidential election will capture the majority of investor attention, in Europe a second wave of COVID-19 cases is rising with the likelihood of increased restrictions that could curtail the trajectory of the regional economic recovery. Additionally, the UK and the EU remain deadlocked in Brexit negotiations with the deadline coming at the end of the year. If a deal is not reached, the UK will exit the EU and its single market trading access. Research by law firm Baker & Mackenzie, estimated a failure to secure a Brexit deal could reduce the UK’s GDP by 3.9% annually over the next decade.

Within emerging markets, we also recommend a neutral allocation with a continued preference toward Asia. Emerging markets outpaced both the U.S. and non-U.S. developed markets during the third quarter driven by the strong rebound in economic activity relative to developed market economies. For example, the China Caixan Manufacturing Index recorded a reading of 53.0 for September, indicating a firm expansion in economic activity. Furthermore, Asian markets continue to benefit from their technology driven composition, as this segment of the economy will continue to drive growth in the new economic landscape. However, emerging markets remain dependent on the developed world and it remains to be seen if the recovery in EM is sustainable given that economic activity in the rest of the world had begun to stall.

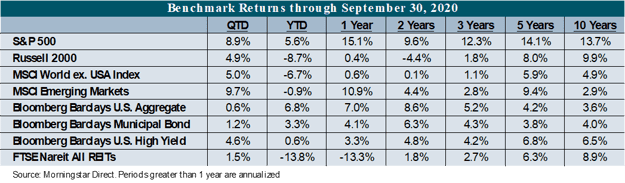

Fixed income markets, measured by the Bloomberg Barclays U.S. Aggregate Index, were up 0.62% for the quarter. Market interest rates were generally stable for the quarter with short, intermediate and long-term Treasury rates ending the quarter within 4 bps of where they started. With Treasury rates anchored to low levels, we continue to allocate to various other fixed income sectors. We are focused on short-term investment grade debt as the intermediate corporate bond index has seen duration increase to over 8.5 years. We also find floating rate debt attractive not only for added yield, but for more stable prices. For instance, in September, high yield bonds fell 1.0% as equity volatility returned but floating rate loans were up 0.6%. Part of this is due to a more muted climb higher from the March lows while high yield has enjoyed a more rapid increase in prices, possibly getting ahead of fundamentals.

Additionally, we have favored municipal bonds since the initial market dislocation occurred in March for multiple reasons. First, relative yields remain elevated and we view credit concerns as overblown. If yields normalize relative to Treasuries, it offers added returns on top of the current yield available. Secondly, the municipal yield curve remains steeper than the taxable yield curve, adding to total return potential through rolldown opportunities. Lastly, the next round of stimulus could provide additional support for state and local governments, easing the optics of potential stress within the asset class.

Our Tactical recommendation includes hedged strategies in U.S. large cap, SMID cap and international equities.

Tax and Financial Planning News

With the 2020 election only weeks away, the time to plan for a potential Presidential administration change is rapidly approaching. While typical year-end income tax strategies may include capital loss harvesting and accelerating deductions such as charitable gifts, in the event of a Biden win and a democratic sweep, strategies for families with greater income may change. If Biden’s tax proposal were implemented, clients with incomes in excess of $400,000, will see higher rates on income over $400,000 and it may be appropriate to take additional measures to recognize elements of income in 2020 to avoid paying higher marginal rates and withholding taxes in 2021. Additionally, with the proposed elimination of the preferential capital gains rate of 20% for those who have more than $1mm of income in 2021, it could make sense to sell highly appreciated stocks or other investments today. As such, capital losses may be more valuable in 2021 than 2020.

For retirees receiving IRA and 401(k) distributions, higher marginal rates may mean higher income taxes in 2021 as well. You may consider taking a larger distribution as we approach year end to cover some of your living expenses in 2021.

The tax implications of a potential administration change extend far beyond the planning strategies listed above. For a review and an understanding of how proposed legislation may affect your personal situation, please contact Robert Davis at robert@roundtablewealth.com.

[i] Philadelphia Federal Reserve Survey of Professional Forecasters, August 14, 2020

*The content herein is provided to you on an as-is basis without any warranties of any kind. In no event shall Owner Resource Group, LLC be liable for any direct, indirect, incidental, punitive, or consequential damages of any kind whatsoever with respect to this content. The content is not intended to provide investment advice. We strongly recommend you consult professional business advisors before making any financial or investment decisions.